PlayAGS Inc, (AGS): Play the Reopening Trade

PlayAGS Inc, (AGS): Play the Reopening Trade

Executive Summary

PlayAGS (AGS) is a supplier of gaming machines, table products, and iGaming content. July’s market sell-off prompted me to take a closer look at the name and I think the market does not fully appreciate the strategic & growth initiatives put in place by the management team:

Their recent entry into the premium gaming machine market could improve revenue/day by over 30%.

New international geographies will help international revenue grow double-digit for the foreseeable future.

Two fast-growing segments with attractive margin profiles provide optionality for investors.

The stock is also well-positioned to benefit from the economic reopening. I see double-digit EBITDA growth for the next 2-3 years and a $30 target price over the long run.

Company Overview

The company reports under three segments.

Electronic Gaming Machines (EGM)

This will be the focus of the story. EGM is the company’s largest segment, representing 91%+ of revenue. To put it crudely, EGMs are modern slot machines. The games are proprietary and developed in-house. AGS generally spends 10-12% of its revenue in R&D to develop new cabinets and games. Its cabinets fall into 2 distinct categories.

Core Cabinets - leased or for sale, include most of their proprietary titles.

Premium Cabinets - Leased only, with high-performing game titles and higher revenue per unit.

AGS either sells the machines outright at an ASP of ~$18,000 or leases the machines. The company takes 15-20% of the casino’s winnings or a flat daily fee through leasing.

Table Products & Interactive

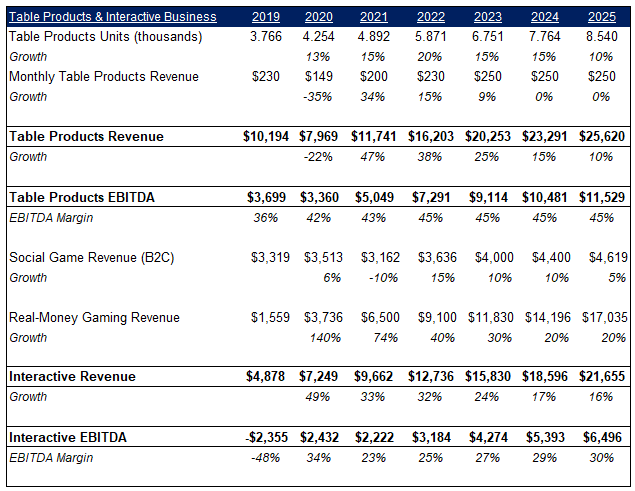

These two segments represent 9% of revenue. I will not spend too much time on them, but these segments provide interesting optionality in the long run.

Table Products include card shufflers, live felt table games, side bets, and other “add-ons” to table games. Side bets are attractive to casinos as the odds for the house are statistically better than your traditional betting games. The table industry has historically been a monopoly, controlled by Scientific Games. However, AGS is rapidly taking market share. I expect continued double-digit growth and market share gains.

Interactive is their B2B & B2C iGaming business. Their B2C business has performed well, but nothing too exceptional. B2B on the other hand is phenomenal. In 2019, the company launched its real-money gaming platform (RMG). If you are familiar with the iGaming sector, think of RMG as BRAGG & GAN. RMG is growing triple-digit and has run-rate revenue of $5.5M. Many of their cabinet games are easily transferable to an online format, creating meaningful synergies between each segment. The company is onboarding 11 new clients in Q2 2021 and is ready to launch in new jurisdictions. In a few years, RMG could be worth AGS’s current market cap.

Competitive Landscape

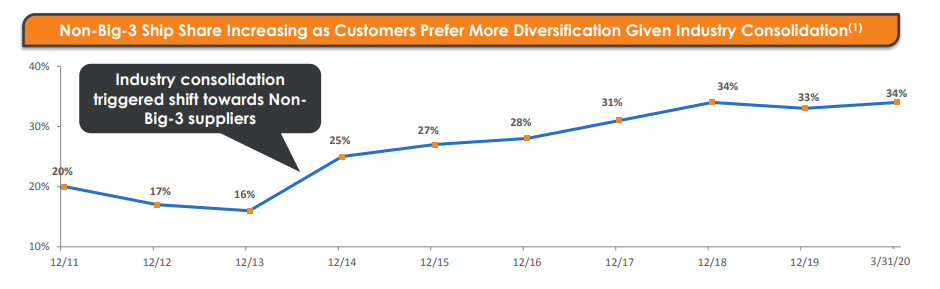

The EGM market is dominated by the “Big Three”: IGT, Scientific Games, and Aristocrat. Together, they control over 65% of the market. Starting in 2013/2014, these players went on a consolidation spree, acquiring important EGM manufacturers (like Bally and WMS). Customers sought to diversify their supplier base by awarding more floor space to smaller manufacturers. As seen in the company’s June 2020 investors presentation, market share from non-Big Three players has grown substantially. I expect this trend to resume as smaller players, like AGS, continue to penetrate the market.

Big Trouble in Little Oklahoma

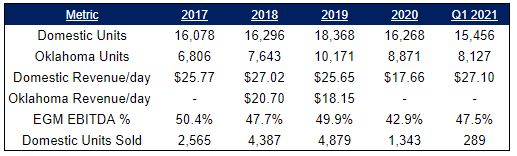

PlayAGS was brought public by Apollo. As you would expect from a PE firm, AGS had a massive amount of debt. Initially, the business performed well, showing improved unit economics and a growing installed base. However, starting in 2019, it faced deteriorating unit economics in Oklahoma. Reasons cited were underperformance from 800 incremental Oklahoma cabinets and severe floods that shut down casinos. Revenue/day/unit (RPD) in Oklahoma dropped substantially and continued to be well below the company’s consolidated average for the remainder of the year. As seen in the table below, Oklahoma represented 55% of its installed base in 2019.

If that was not enough, COVID hit when management initiated several strategic initiatives. With a ton of debt and clients closed indefinitely, the stock plummeted.

Strategic Initiatives

AGS’ management team worked tirelessly in 2020 to stabilize their business and position it for growth.

They used COVID as an opportunity to reset their installed base. By extensively looking at the ROIC of each cabinet, lower-yielding units were promptly identified and pruned out of their client’s casinos. In total, the company sold 1300 lower-yielding units, primarily in Oklahoma. This initiative should improve domestic RPD and reduce unnecessary CAPEX moving forward.

The company also launched its new Orion Starwall premium EGM and is set to launch a new Orion Curve premium package in the back half of the year. These machines generate higher levels of engagement and better RPD. The management team has a lot of room to improve their domestic RPD, which is currently the lowest in the sector as seen in the picture below. I will spend a little bit more time on this initiative in the following section through a case study of Everi.

Mini Case Study - Everi (EVRI)

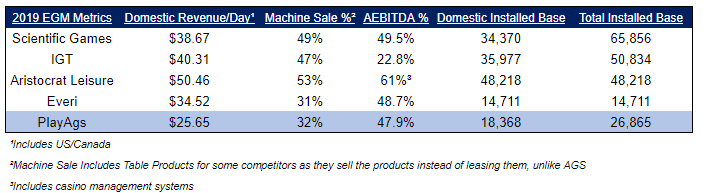

Everi used to serve primarily the core cabinets market and both companies had similar RPD. EVRI, however, made an aggressive push to penetrate the premium market. As seen in the picture below, Everi’s premium cabinets installed base grew significantly from 2,859 in 2018 to now 6,478. RPD grew from $28.42 to a peak of $34.52 before falling in 2020 due to COVID.

Similarly, AGS started to focus on the premium market in late 2019/2020. Management estimates that the premium market contains 70,000 cabinets. As of Q1 2021, the company only had 400 Orion Starwall cabinets installed, representing a 0.6% market share. As the company progresses through its strategic initiative, I would expect RPD to grow substantially, hitting a new high in 2022. Their Q1 2021 results have already shown considerable improvement from 2019 levels. If AGS can re-produce what Everi accomplished, we are looking at a 30-40% uplift in RPD over the next few years.

White space Opportunities & Catalysts

PlayAGS has quite a few interesting white space opportunities both domestically and internationally.

In Q4 2020, the company sold its first Historical Horse Racing (HHR) cabinet in Kentucky. The momentum continued in Q1 2021 with 65 additional cabinets going live. HHR units allow individuals to bet on past horse races (details of the race are presented in an anonymized way). By scouring through the Kentucky Horse Racing Commission’s reports, one can see massive growth in bets handled in 2020 and 2021. This is also true for prior years. Currently, only Virginia and Kentucky permit HHR. Management believes 2 new jurisdictions might legalize HHR in the coming 12 months.

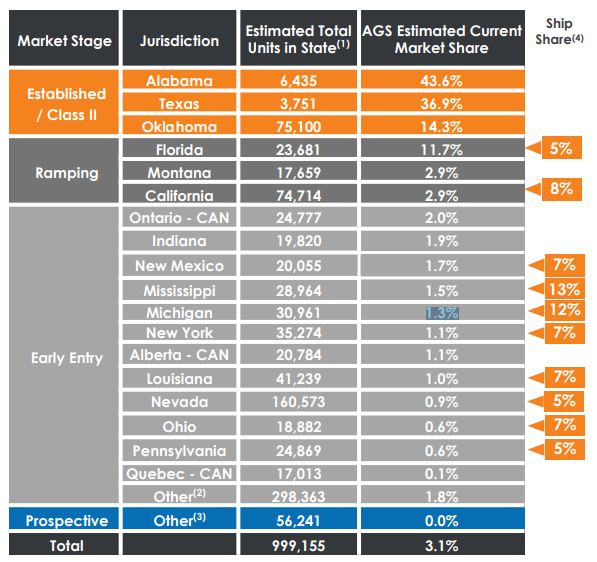

The company’s installed base is highly concentrated in three geographies: Alabama, Florida, and Oklahoma. Pre-COVID, the company was expanding in new states. Its ship share, which is the % of total units sold attributable to AGS, outpaced its market share by a wide margin in nine states. Some people believe this trend might not be the same post-COVID, but I simply do not see any structural or fundamental issues that would prevent the company from taking market share.

International geographies are also an area of growth for the company. International revenue was growing significantly in 2019 (53%) and accounted for 15% of total revenue. The management team was making strides in new geographies. This included the Philippines, Argentina, Peru, and Asia. I see this trend resuming in the back half of 2021 as these economies re-open.

Additional short-term opportunities/catalysts include:

AGS is clearly a reopening trade and I would expect EGMs utilization to remain high for the remainder of the year as consumers unleash their wallets. Given their revenue share arrangement, AGS should directly benefit from this.

At the height of the pandemic, the management team took the prudent approach to shore up liquidity by taking out a $95M loan. Unfortunately, the interest rate was not advantageous at LIBOR+13%. The loan is likely to be refinanced in May 2022 at a much lower rate. For comparison, their two other loans bear interest rates of LIBOR+3.5%.

Competitive Positioning

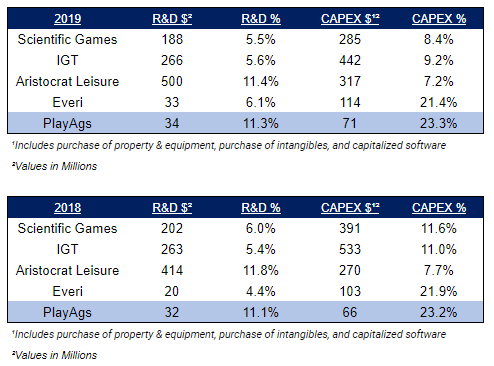

Why am I so confident that PlayAGS can continue taking market share? Being a smaller player, AGS has needed to rely on innovation to gain an edge. As seen on the tables below, the company consistently spent more on R&D than its competitors relative to its top-line.

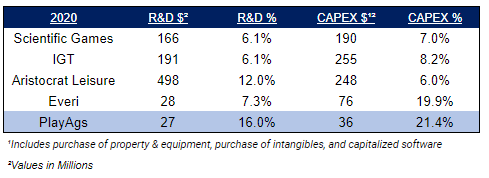

This continued to be true for 2020 as well.

I realize that R&D does not always translate into results. However, this metric, coupled with their previous ship rates, seem to indicate some sort of success. Naysayers will proclaim that bigger players spend 5-10x more on an absolute basis. I would argue history has consistently shown that smaller players can uproot incumbents by innovating.

Valuation

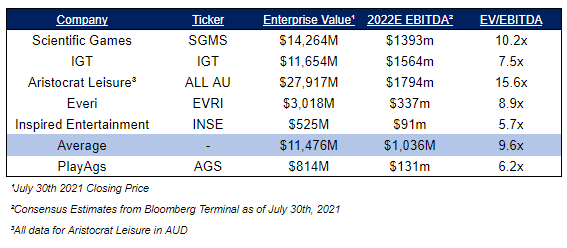

It is an interesting point in time to look at PlayAGS following July’s sell-off. Recall that the stock reached a high of $11.32 before dropping to its current levels. Currently, the stock trades at a discount to all other major players in the space. A discounted multiple is warranted given:

Their 2019 debacle (and its leverage)

Competitors are more diversified with interesting and bigger adjacent segments.

That said, I expect the multiple to slowly improve as the company progresses through its strategic initiatives. In addition, the growing Table Products & Interactive segments should provide valuation support.

Bloomberg’s 2GY EV/BEst EBITDA chart (Estimates on 2022’s EBITDA) shows a multiple that compressed from close to 11x at its peak to now 6.3x. In fact, AGS’s multiple was higher than many of its comparables before 2019. Note that the Bloomberg data differs from the previous table given a difference in diluted share count.

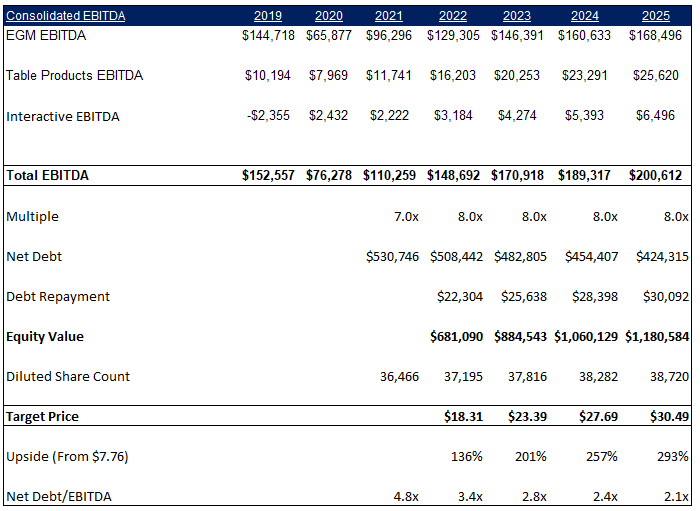

I won’t make a case for the multiple to return to 2018’s levels. But, let’s look at a scenario where everything works out as I would hope: The company’s multiple returns to 8x, RPD grows meaningfully and EBITDA margins return to 2019 levels.

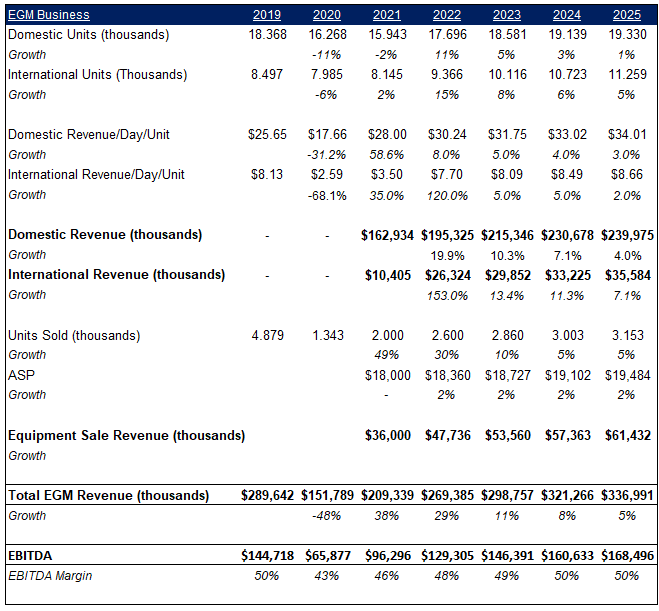

For Table Products, I forecast decelerating double-digit revenue growth with stagnating margins over the forecast period as the company continues to take market share from Scientific Games. For Interactive, I assume high double-digit revenue growth and margins expansion to 30% by 2025. This seems reasonable given the industry is in its early innings.

With these assumptions, I get to $18.31 off of 2022’s numbers. The 5-year target price gets us to a three-bagger.

Obviously, the above scenario could prove to be wrong. As such, I modeled a “subdued” scenario. EBITDA for the EGM segment is forecasted to return to 2019’s levels in 2025. I reduced my numbers for both the Table Products & Interactive segment and kept the company’s multiple at 7x EBITDA.

As you can see, I am not really shooting for the stars here. AGS has an interesting upside despite conservative assumptions. Reality will likely fall in between my two scenarios.

Key Risks

Slot machines have been in a secular decline for a while. Lower interest from younger generations, growth in alternative gambling (like sports betting), and the proliferation of online gambling are all contributing to this trend. While I do think this is likely to continue, AGS can continue to grow by taking market share. And, with an embedded option in two attractive segments, the risk seems to be worth taking.

The company currently has 531M of net debt. TTM net debt/EBITDA stands at 7.4x. Obviously high, but distorted by the impact of COVID. If one uses 2019’s EBITDA, the company stands at 3.6x, which is manageable. I also believe the recurring nature of their business allows for a higher debt load. The company’s CEO has made it clear that debt reduction will be a priority coming out of COVID.

Apollo still holds 21.7% of the shares outstanding. I usually dislike investing in firms with a PE overhang. However, the company filed a secondary offering on July 2nd for the totality of the shares held by Apollo. They should be exiting imminently.

COVID delta variant. Yes, we aren’t done with COVID, unfortunately. Masks mandates are being re-implemented and there is a risk that restrictions could follow.

Closing Remarks

The company is scheduled to release its Q2 2021 results on August 5th. I want to emphasize that PlayAGS is NOT a Q2 2021 earnings play. The results should be good given incremental casino reopenings and growing tourism. However, there are still uncertainties surrounding the delta variant and demand for cabinets.

Finally, I want to thank everyone who took the time to read this article. If you like the content I publish, please take a moment of your time to subscribe and follow me on Twitter @InflexioSearch

Disclaimer: I am long AGS. The information contained above is not and should not be construed as investment advice, and does not purport to be and does not express any opinion as to the price at which the securities of any company may trade at any time. The information and opinions provided herein should not be taken as specific advice on the merits of any investment decision. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

thank you